15 mins read

Whether you’re building an emergency fund, investing for the future, supporting children or grandchildren, or thinking about passing on wealth, ISAs can play an important role in your financial plans.

Over time, tax rules and allowances can change. But the core benefits of ISAs remain valuable:

tax-efficient growth

flexibility

long-term planning opportunities

and simplicity compared with many other financial products

Why ISAs still matter

ISAs remain one of the most flexible and tax-efficient ways to save and invest for the future. Some people assume ISAs have become less important in recent years because of the Personal Savings Allowance. However, ISAs can still provide significant long-term value, particularly for investors and higher-rate taxpayers. Unlike many other savings and investment accounts, money held within an ISA can benefit from:

no UK Income Tax on interest or investment returns

no Capital Gains Tax

no Dividend Tax

no need to declare ISA growth on a tax return

As tax allowances have reduced in recent years and more people are paying higher rates of tax, ISAs have become increasingly important as part of wider financial planning. For many people, ISAs are not simply savings accounts. They are long-term planning tools that can support:

retirement income

investing for children

inheritance planning

medium and long-term financial goals

and tax-efficient investing alongside pensions

“ISAs remain one of the simplest and most flexible ways to save and invest tax-efficiently.”

ISA type | Best for | Time horizon | Risk level |

|---|---|---|---|

Cash ISA | Emergency savings | Short-term | Lower |

Stocks & Shares ISA | Long-term growth | 5+ years | Medium to higher |

LISA | First homes/retirement | Long-term | Varies |

Junior ISA | Children's future | Long-term | Varies |

Understanding your ISA allowance

In the 2026/27 tax year, most adults can contribute up to £20,000 across ISAs. You can split this allowance across different ISA types, including:

Cash ISAs

Stocks and Shares ISAs

Lifetime ISAs

Innovative Finance ISAs

For example, you might choose to hold part of your allowance in cash for short-term needs, while investing the remainder for longer-term growth. The allowance resets each tax year and cannot be carried forward if unused.

“ISA allowances cannot be carried forward, which means unused allowances are lost each tax year.”

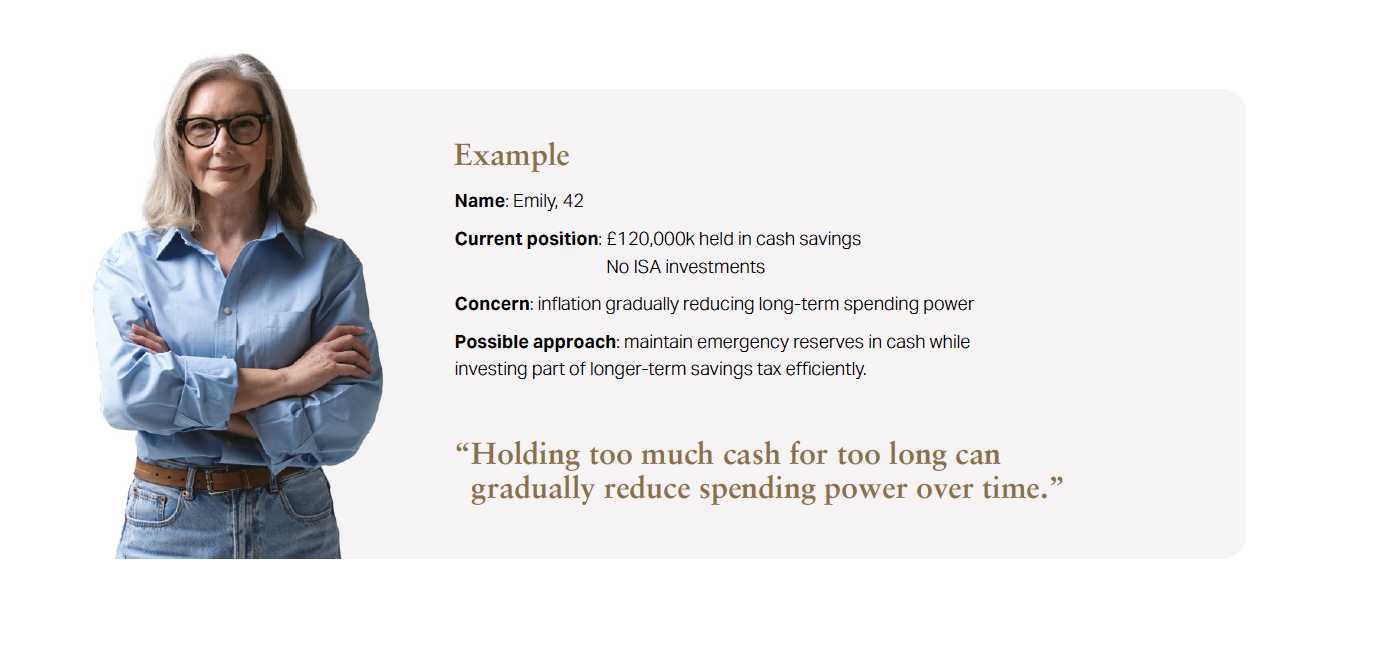

Holding cash vs investing

Deciding whether to save or invest is often one of the most important long-term financial planning decisions. Cash savings can provide stability, accessibility and reassurance for short-term goals. However, inflation can reduce the spending power of cash over time. For example, if inflation averages 3% per year, the real value of money held entirely in cash may gradually fall if interest rates do not keep pace.

Investing involves risk, and the value of investments can rise and fall. But over the long term, investing has historically offered greater potential to outpace inflation and grow wealth in real terms. In practice, many people use a combination of both: cash for shorter-term needs and emergency reserves and investments for longer-term goals. A useful rule of thumb is:

short-term goals often favour cash

long-term goals may benefit from investing

The appropriate balance will depend on your objectives, time horizon, attitude to risk and wider financial circumstances.

“Holding too much cash for too long can gradually reduce spending power over time.”

Choosing the right ISA for you

There is no single “best” ISA. The right option depends on what you want your money to achieve.

Cash ISA

A Cash ISA works similarly to a traditional savings account, with the added benefit that interest earned is free from UK Income Tax. Cash ISAs can be suitable if you:

need easy access to money

are building an emergency fund

are saving for short-term goals

or prefer lower levels of risk

There are different types of Cash ISA available, including:

easy-access accounts

fixed-term accounts

and notice-based accounts

Some offer higher interest rates in exchange for reduced flexibility.

Important considerations

While Cash ISAs can provide security and stability, it’s important to consider the effect of inflation over time. If savings growth does not keep pace with rising prices, the real value of money may gradually reduce. For this reason, holding large amounts in cash over long periods may not always support long-term financial goals.

When might a Cash ISA be suitable?

Emergency savings

Short-term spending goals

Planned purchases within the next few years

Clients who prioritise stability over growth potential

“Cash can provide stability and accessibility, but inflation may affect long-term purchasing power.”

Stocks and Shares ISA

A Stocks and Shares ISA allows you to invest tax-efficiently for medium to long-term goals. Rather than holding cash, investments may include:

funds

shares

bonds

and other qualifying investments

Any growth or income generated within the ISA is free from UK Capital Gains Tax and Dividend Tax.

Investing for the long term

Investing should generally be viewed as a long-term commitment. Markets naturally rise and fall over time, and short-term volatility is a normal part of investing. However, remaining invested for longer periods has historically improved the likelihood of positive returns. For many people, a Stocks and Shares ISA can support goals such as:

retirement planning

building long-term wealth

future lifestyle planning

or investing excess cash more efficiently

Understanding risk

All investments carry risk, and you could get back less than you invest. The appropriate level of investment risk will depend on your goals, time horizon, financial resilience and attitude towards market fluctuations.

A well-structured investment portfolio should reflect your individual circumstances rather than short-term market movements.

When might a Stocks and Shares ISA be suitable?

Long-term financial goals

Investing over five years or longer

Retirement planning

Building wealth gradually over time

“Investment risk is not simply about market movements, it’s also about whether your money can keep pace with inflation over time.”

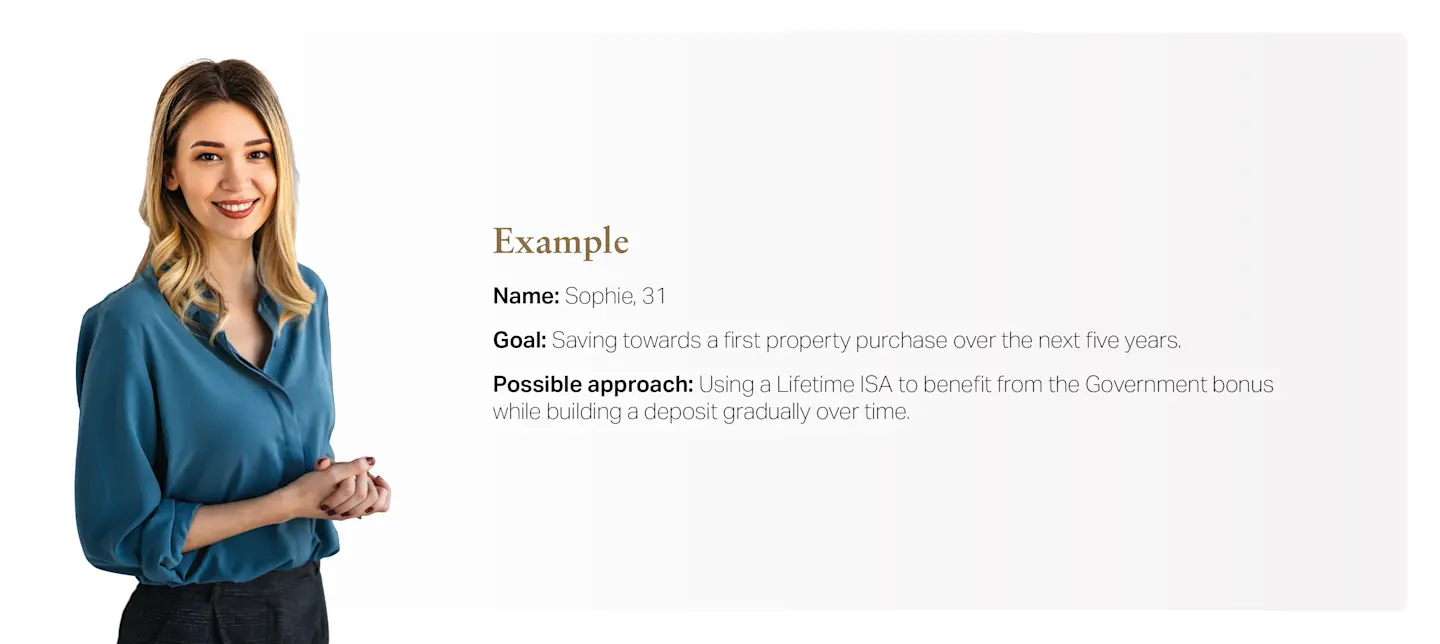

Lifetime ISA (LISA)

The Lifetime ISA was designed to support first-time buyers and long-term retirement savings.

You can open a Lifetime ISA between the ages of 18 and 39 and continue contributing until age 50.

Up to £4,000 can be contributed each tax year as part of your overall ISA allowance.

The Government currently adds a 25% bonus to contributions, meaning a maximum annual bonus of £1,000 may apply.

Important restrictions

Money can usually be withdrawn without penalty only if:

purchasing a qualifying first home

or from age 60 onwards

Withdrawals for other reasons may trigger a withdrawal charge, meaning you could receive back less than you contributed.

Is a Lifetime ISA right for everyone?

Not necessarily. While the Government bonus can make a LISA attractive for some people, pensions may offer greater long-term tax advantages in certain circumstances, particularly where employer contributions are available. The right approach depends on your wider financial plans and objectives.

When might a Lifetime ISA be suitable?

Saving for a first property purchase

Supplementing retirement savings

Long-term disciplined saving goals

“For some people, a lifetime ISA can provide a valuable boost towards long-term savings goals.”

Junior ISA

A Junior ISA allows parents or guardians to save or invest on behalf of a child in a tax-efficient way. In the 2026/27 tax year, up to £9,000 can be contributed into a Junior ISA. There are two main types:

Cash Junior ISA

Stocks and Shares Junior ISA

Building for the future

Junior ISAs are often used to support future goals such as:

university costs

first home deposits

driving lessons

or providing a financial foundation in adulthood

The account belongs to the child, and they can take control of it from age 16. Withdrawals are generally not possible until age 18. Because of the long-term time horizon involved, some families choose to invest through a Stocks and Shares Junior ISA to provide greater growth potential over time.

Family contributions

Parents, grandparents and wider family members can all contribute towards a Junior ISA, making them a useful intergenerational planning tool.

When might a Junior ISA be suitable?

Long-term saving for children or grandchildren

Building wealth gradually over many years

Gifting money tax-efficiently for future use

“Starting early can make a meaningful difference over time.”

Existing Help to Buy ISAs Help to Buy ISAs are no longer available to new applicants. However, if you already hold one, you may continue contributing subject to existing rules and deadlines. Some individuals may choose to transfer existing Help to Buy ISA savings into another ISA arrangement, depending on their circumstances and objectives. |

|---|

Can you transfer an ISA?

Yes. In many cases, ISAs can be transferred between providers without affecting your annual ISA allowance.

People often transfer ISAs to:

consolidate older accounts

access different investment options

improve flexibility

or align accounts more closely with current goals

Important. ISA transfers should normally be completed using the provider’s formal transfer process. Withdrawing funds yourself and reinvesting them separately may unintentionally affect your ISA allowance or tax position.

“Reviewing older ISAs regularly can help ensure they still reflect your goals and priorities.”

Using ISAs as part of wider financial planning

ISAs are often most effective when viewed alongside wider financial planning considerations. For example, they may complement:

pensions

retirement income strategies

inheritance planning

emergency reserves

and intergenerational gifting

For couples, each person has their own ISA allowance. This means families can potentially shelter significant amounts tax-efficiently over time. Used consistently over many years, ISAs can become an important part of long-term wealth planning.

Passing ISAs to loved ones

ISAs can also form part of estate and inheritance planning. If ISA assets are left to a surviving spouse or civil partner, the Additional Permitted Subscription (APS) rules may apply. This allows the surviving partner to inherit an additional ISA allowance based on the value of the deceased partner’s ISA holdings. However, it’s important to remember:

ISAs are not automatically free from Inheritance Tax

and different rules may apply depending on who inherits the assets

Because inheritance planning can be complex, professional advice may help ensure arrangements remain aligned with your wishes.

“ISAs can play an important role not only in wealth creation, but also in passing wealth between generations.”

Common mistakes to avoid |

|---|

- Leaving large sums in cash for long periods without reviewing inflation impact - Accidentally withdrawing ISA funds instead of transferring them formally - Focusing only on short-term market movements - Forgetting to use annual ISA allowances - Holding investments that no longer reflect your goals or attitude to risk |

Common questions

Can I have more than one ISA?

Yes. You can hold multiple ISAs, although contribution rules apply.

Can I withdraw money from an ISA?

Usually yes, although some products may have restrictions or penalties.

Are ISAs risk-free?

Cash ISAs are generally lower risk. Investments held within Stocks and Shares ISAs can rise and fall in value.

Do I pay tax on ISA growth?

Under current UK tax rules, growth and income generated within an ISA are generally tax-free.

Can I inherit an ISA?

Specific rules apply depending on your relationship to the deceased and the type of ISA involved.

When advice can help

Financial planning is rarely about one product in isolation. ISAs are often most effective when they form part of a wider long-term plan built around your goals, priorities and circumstances:

how much to hold in cash versus investments

appropriate investment risk

retirement planning

tax-efficient income strategies

inheritance planning

and long-term family wealth planning

At Succession Wealth, we help clients build financial plans designed around their individual goals, priorities and circumstances.

“The right financial plan should reflect your goals, priorities and circumstances – both now and in the future.”

This guide is for general information only and does not constitute advice. The information is aimed at retail clients only. Tax treatment depends on individual circumstances and may change in future.

The value of your investment(s) and the income derived from it, can go down as well as up and you may not get back the full amount you invested.

Succession Wealth is a trading style of Succession Wealth Management Limited, which is authorised and regulated by the Financial Conduct Authority. Financial Services Register number 588378. Succession Wealth Management Ltd is registered in England and Wales at The Apex, Brest Road, Derriford Business Park, Derriford, Plymouth PL6 5FL. Registered Number 07882611.

FP2026-XXX - last reviewed July 2026